HOME | BIO | RESEARCH WORK | TEACHING | NAPLES | SOCCER

PAOLO PASQUARIELLO

ppasquar@umich.edu John C. and Sally S. Morley Professor of Finance

Ross School of Business, University of Michigan

ACADEMIC APPOINTMENTS: Ross School of Business, University of Michigan Universita' Ca' Foscari, Department of Economics Stockholm School of Economics, Swedish House of Finance (SHOF) ADDITIONAL APPOINTMENTS: Journal of Financial Markets Review of Financial Studies EDUCATION: Stern School of Business, New York University Universita' Commerciale Luigi Bocconi

RESEARCH INTERESTS (read more) :

MAIN PUBLICATIONS (read more) : Review of Corporate Finance Studies internet appendix )

Journal of Finance Journal of Financial and Quantitative Analysis internet appendix )

International Journal of Public Health https://doi.org/10.1007/s00038-020-01399-y

Journal of Financial and Quantitative Analysis internet appendix )

Review of Financial Studies internet appendix )

Review of Finance Review of Financial Studies Michael J. Brennan RFS Best Paper Runner-Up Award ).

(The MDI series over 1973-2009 is available on request; more detailed

information on and analysis of the ADR subsample are in Pasquariello (2018) )

Journal of Economic Theory typos )

Real Estate Economics Journal of International Money and Finance Liquidity PhenomenonJournal of Financial Economics Lead Article ).

Review of Financial Studies SSRN )

Journal of Financial and Quantitative Analysis Lead Article ).

Journal of International Economics Journal of Financial Markets Journal of Empirical Finance Review of Financial Studies Review of Financial Studies here )

Journal of Financial Markets Lead Article ).

(typos )

Journal of Business Real Estate Economics WORKING PAPERS (read more) : SELECTED MEDIA MENTIONS & INTERVIEWS: Nasdaq, S&P 500 update stock lists to reflect today’s market APR-Marketplace click to listen )

Xi meets Brazil's Lula amid calls to shake up Western-led order Nikkei Asia One Month from Silicon Valley Bank’s Collapse: What Now? TRT World Research Centre SVB, Credit Suisse, and contagion: When ignorance isn't bliss The Hill Office Hours: Paolo Pasquariello on Inflation Michigan Alum Death, taxes and national income identities: A frightening tale for the British pound The Hill Why it's time to start paying with $2 bills CNN.com Flat tax “indifendibile”: farebbe esplodere il deficit pubblico FIRST online Is Biden or Bezos right about gas prices? Economists weigh in Fortune Какой могла бы стать российская экономика за 20 лет Voice of America Como EUA e Brasil enfrentam alta da gasolina BBC Brasil The Treasury Department bars Americans from buying Russian stocks The New York Times Se espera que entre los temas presentes esté el aumento en los precios de alimentos y combustibles, así como el cambio climático y los efectos de la pandemia El Mercurio Кому на Руси будет жить хорошо? Voice of America Gas prices rapidly increase as conflict overseas persists longer than expected ABC 12 News Храните деньги в сберегательной кассе? Voice of America Russia-Ukraine war: What to know about sanctions—their effects and effectiveness University of Michigan News Sanções dos EUA pelo mundo têm impacto limitado, mas exemplo efetivo no Irã Fohla de Sao Paulo Curva de juros dos EUA volta a se inverter e aumenta temor de recessão Agência Estado For Companies Still Selling in Russia, ‘Essential’ Is a Loose Term The Wall Street Journal Sanções econômicas funcionam? O que a história diz sobre o sucesso dessas medidas BBC Brasil French , Spanish ), March 20, 2022.

Ukraine-Russia crisis: What to know about decisions by global business players as war rages University of Michigan News Michigan companies exit Russia, but Kremlin threatens countermeasures The Detroit News U-M professors and students discuss economic impacts of Russia invading Ukraine Michigan Daily U-M community reacts to invasion of Ukraine, experts weigh in Michigan Daily Michigan gas prices are soaring. Who’s to blame, when will it stabilize? Bridge Michigan What exactly is the SWIFT banking system? APR-Marketplace When risk and uncertainty abound, investors move to government bonds in a “flight to safety” APR-Marketplace click to listen )

Here's how Russia's invasion of Ukraine could impact Michigan's economy ABC-WXYZ Detroit click to watch )

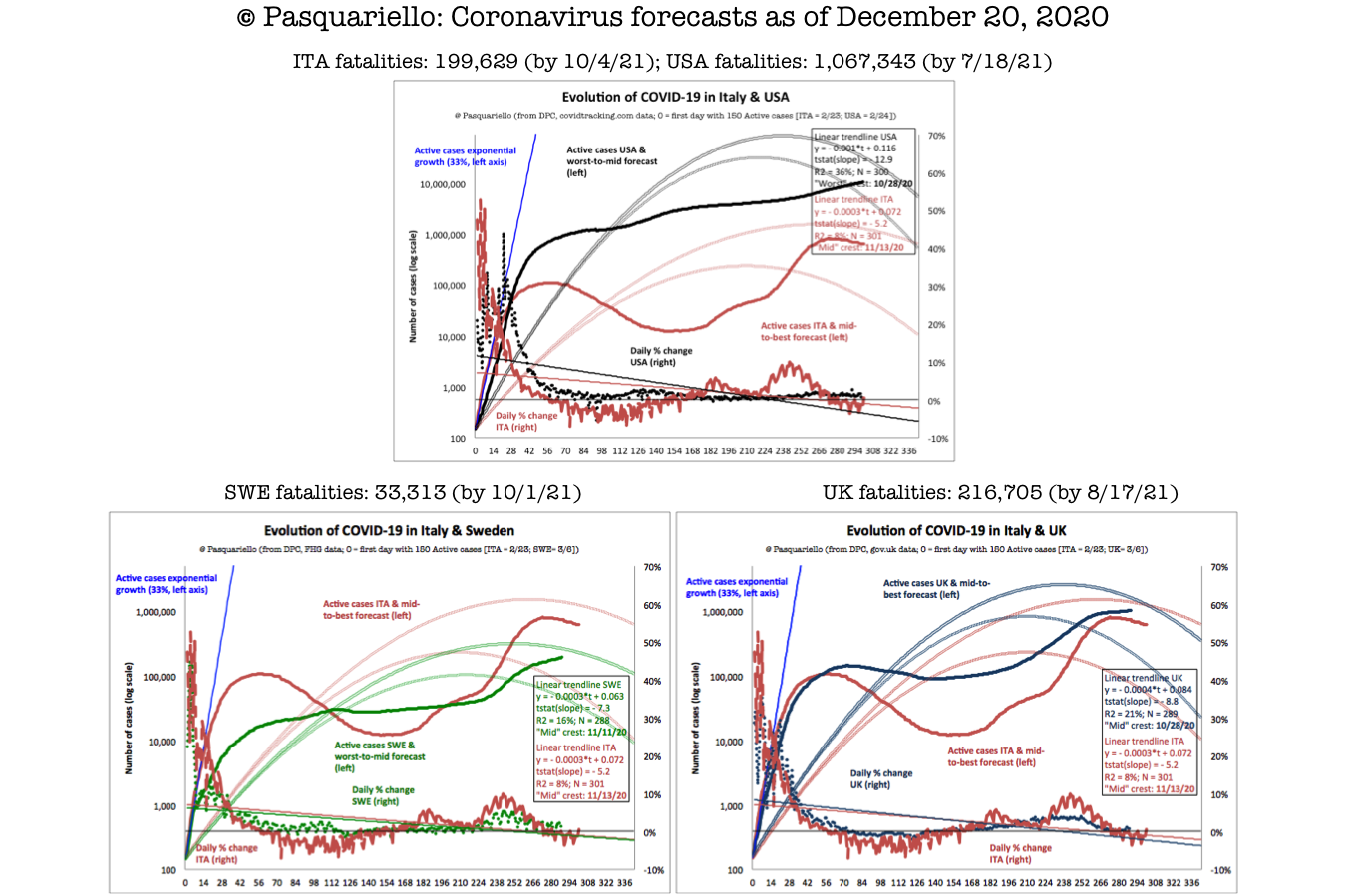

Expect High Prices, Slowed Down Recovery If Ukraine Conflict Continues MIRS News Michigan gas prices are climbing. Experts are now keeping an eye on Russia MLive.com Automakers, Michigan businesses brace for supply chain impacts from Russia sanctions The Detroit News Ukraine-Russia crisis: What to know about the potential fallout for global financial markets University of Michigan News Why the state lottery stayed successful during the pandemic, while other entertainment businesses struggled Michigan Advance Il caso Archegos: perché non è come LTCM Class CNBC Rocket Companies stock soars 70% on speculative trading, mirroring GameStop rally Detroit Free Press GameStop et Reddit: révolution à Wall Street Pour l'Eco GameStop gamers battle risk in fight against Wall Street Detroit Free Press How to Invest Money: Make Your Money for You CreditDonkey.com Con i mercati sotto pressione non sempre il prezzo e' giusto IlSole24Ore India Inc's Rising Cost of External Capital Business Today Money Moves for Recent Grads InvestorPlace Remessas de brasileiros nos EUA caem até 90%, mas podem aliviar auge da crise no Brasil BBC Brasil U-M experts imagine aspects of life, lessons learned after coronavirus University of Michigan News Nos EUA, pagamento de auxílio emergencial será feito com crédito em conta ou pelo correio O Globo Financial, economic actions during crisis may be rational, if not ethical University of Michigan News Flexibilização é ameaça ao sistema, dizem especialistas Valor Economico Are U.S. consumers especially suspicious of internationally based banks? WalletHub.com China’s Coronavirus Highlights the Risks of a Changing Oil Industry Investorplace.com Investors show Trump, Xi what they think of their trade war The Hill Will Political Uncertainty Trump Financial Markets? CFO Magazine Brexit Vote Stokes Middle-Market Concern Middle Market Growth Hillary Clinton vs. Donald Trump: here’s how Wall Street sees it U.S. News & World Report Greece's financial crisis won't deter travels, but could impact local biz Crain's Detroit Why the Greek Crisis is Unlike Anything You Saw with Lehman Brothers TheStreet.com Euro-Free Greece: Hyper-Inflation, Shrinking Real Wages and Demand, and Unemployment Newswise.com Can You Still Trust These Economic Indicators? CNBC La saggezza (dubbia) dei mercati finanziari Corriere della Sera Perche' tutti vanno all'assalto del keynesismo monetario di Ben Bernanke Il Foglio Warren: New Consumer Bureau Will Help Students Michigan Daily 'Flash Crash' Poses Further Uncertainty for Stocks Business Week L'inflazione ai minimi Il Riformista Financial Crisis Panel Ross School of Business Crisis has hit home, University of Michigan experts say Ann Arbor News Stock Market Crash: Understanding the Panic Business Week Il "pacchetto Paulson" e la democrazia alle corde NewsItaliaPress Tremonti: Speculazione finanziaria? "La peste del secolo" NewsItaliaPress Stocks: A Place Called Vertigo Business Week Remembering Black Monday CIO Magazine Lessons from the ’87 Crash Business Week Markets: Keeping the Bears at Bay Business Week MY INTERNATIONAL FINANCE COURSE BLOG: Lecture 1: Globalization is here to stay Lectures 2 to 24 on LinkedIn MY FORECASTS & COMMENTS ON THE CORONAVIRUS CRISIS: Facebook: My daily COVID-19 model-based forecasts & commentary for Italy, United States, Sweden, & United Kingdom LinkedIn: The revenge of pandemic zombies? LinkedIn: Pandemic zombie ideas are out in force, again LinkedIn: The (measurable) cost of (pandemic) stupidity LinkedIn: Italy wins the Euros ... & the vaccination race LinkedIn: One-liners to the unvaccinated LinkedIn: (Pandemic) politics can kill you LinkedIn: All that glitters is not pandemic gold LinkedIn: What does Juventus have to do with Covid-19 vaccines? Nothing, and that's the point LinkedIn: Excess mortality in Italy in 2020 LinkedIn: Are there moral victories in pandemic fights? LinkedIn: Mr. Draghi, the time to act on the pandemic is now LinkedIn: The U.S. is entering a dark coronavirus winter LinkedIn: A simple model to predict when Italy will enter a national lockdown LinkedIn: Johnson & Trump, brothers in pandemic failure LinkedIn: Teaching in a pandemic LinkedIn: The EU pandemic failure LinkedIn: The U.S. pandemic failure LinkedIn: Poverty, race, violence, and hypocrisy in coronavirus times LinkedIn: The coronavirus-David versus modern society-Goliath LinkedIn: Debt hawks as false prophets in coronavirus times LinkedIn: Deadly zombie ideas in coronavirus times LinkedIn: Short-termism and the coronavirus LinkedIn: The dubious economics of reopening the economy too early LinkedIn: The tragic power of simple narratives and stereotypes LinkedIn: Being ethical or being good against the coronavirus? LinkedIn: Germany's (latest) leadership failure LinkedIn: Governments as deus ex machina dropping money LinkedIn: Some thoughts on the number of COVID-19 deaths in Italy LinkedIn: A (bank) run on toilet paper? LinkedIn: The ECB comes up short (again) LinkedIn: Should governments manipulate stock prices? LinkedIn: Managing (or ignoring) risk in times of coronavirus LinkedIn: Are there winners (and losers) in times of coronavirus? Ross Commentary on Finance: Trying to make (economic) sense of the coronavirus crisis MY MUSINGS ON THE 2011 FINANCIAL CRISIS IN EUROPE: Eyes on Europe MY OTHER WEBPAGES: Google Scholar SSRN EconPapers IDEAS LinkedIn MISCELLANEA: Third Conference on Sovereign Bond Markets Fireside Chat between Marti Subrahmanyam and Chairman Paul Volcker Co-Organizers: Paolo Pasquariello and Marti Subrahmanyam MORE (OR LESS) SERIOUS INFORMATION ABOUT ME: Paolo Pasquariello parla del mondo della finanza, del sistema accademico italiano e americano

e delle crisi economiche e finanziarie globali (in Italian) +39 Podcast Twenty Questions Dividend

________________________________________________________________________________HOME | BIO | RESEARCH WORK | TEACHING | NAPLES | SOCCER